This article is part of a larger series on Business Financing.

TABLE OF CONTENTSA Dun & Bradstreet Business Credit Report, also known as a D&B Credit Report, is a report sourced by credit bureau Dun & Bradstreet that collects data to determine a company’s creditworthiness and financial standing. Generally, it includes company information, payment history, trade references, credit scores, and ratings among other company details. It is utilized by potential lenders, business partners, or vendors in due diligence to evaluate the financial strength and credit risk of your business. These reports can be generated by a third party or created by you for your business.

Not only are business credit reports accessible to lenders or partners, but they also allow you to demonstrate your creditworthiness and later use it to your advantage. This includes leveraging your profile for better lending terms, payment schedules, and more.

It may be for you if you are a business:

There are many elements to decipher when reading a D&B credit report. Here are some key features to look out for.

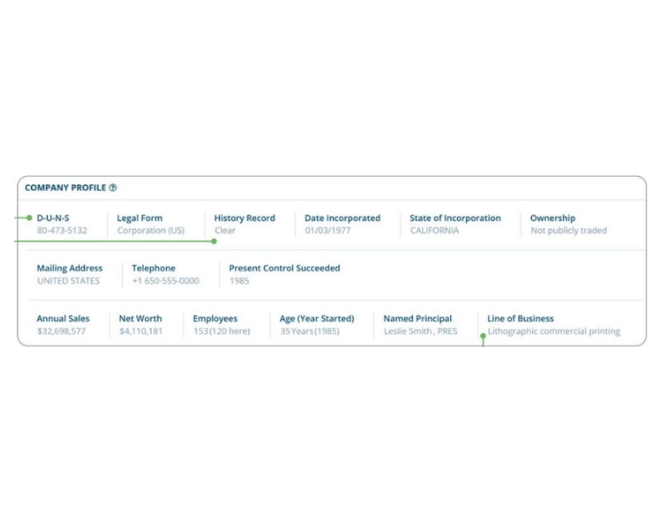

The company profile section summarizes key company details, such as your DUNS Number, contact information, industry classification, and business structure. It can be utilized to verify and assess your business by lenders, partners, or vendors.

Company profile section of a D&B profile.

Categories of company profile section.

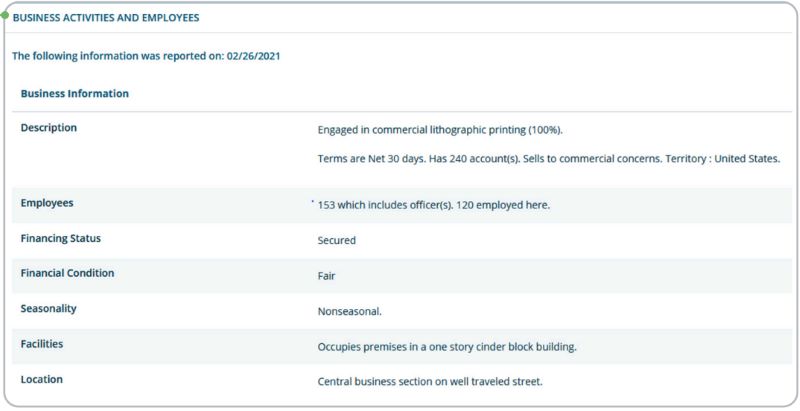

This section is attached to the company profile and includes information regarding your business description, number of employees, financial status and condition, payment terms, seasonality, and location and facilities.

Business Activities section of a D&B profile.

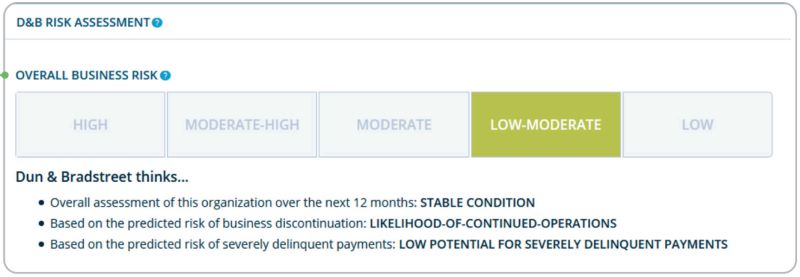

Scores provided by D&B are evaluated by several factors used to determine the potential risk and creditworthiness of a business. In measuring overall business risk, there are five scores, ranging from low to high, along with insight provided by D&B as to the present and future financial strength of your business.

Risk assessment section of D&B profile.

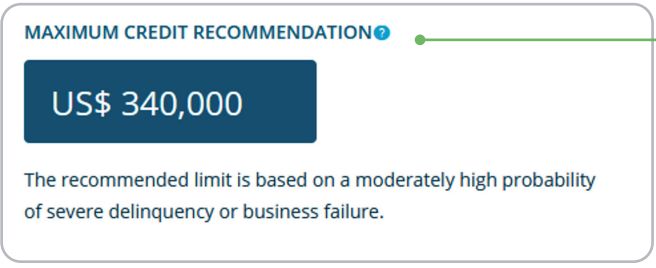

Also included is D&B’s Maximum Credit Recommendation, which is the suggested maximum amount of credit to be extended to your business.

Maximum credit recommendation of a D&B profile.

There are five ways in which D&B measures your score:

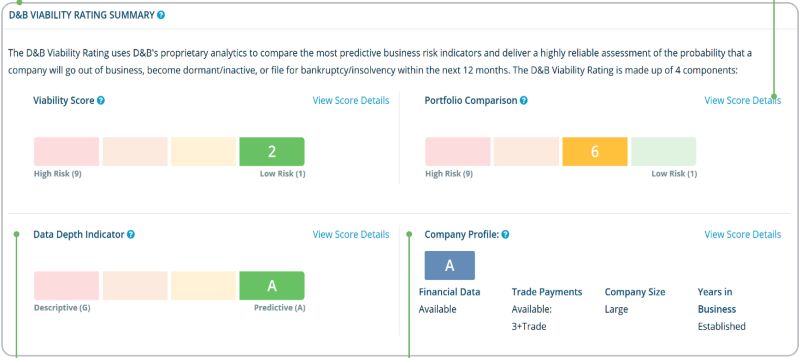

1. Viability RatingA viability rating is based on the risk that a company will no longer be in business, file for bankruptcy, or become inactive within a 12-month period. The rating is made up of four components—including viability score (scores ranging from 1 to 9; 1 being the lowest risk), portfolio comparison (scores also ranging from 1 to 9; 1 being the best in comparison), data depth indicator (scores ranging from A to M), and company profile (scores ranging from A to Z).

Viability rating scoring model.

2. D&B Delinquency ScoreThe D&B Delinquency score ranges from 1 to 100 and represents the probability that a company will be delinquent in making payments, generally 90 days or later.

D&B Delinquency Score model.

3. D&B Failure ScoreThe D&B failure score ranges from 1 to 100 (1 being the highest risk) and determines the likelihood that creditors won’t receive payment if a company fails, including filing for bankruptcy or going out of business.

D&B Failure score model.

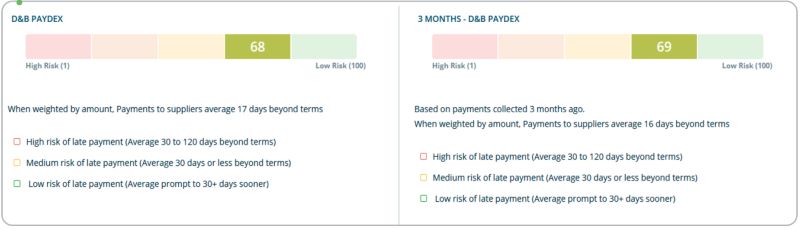

4. PAYDEX® ScoreA PAYDEX ® score is calculated by the performance of a business’s payment history over the past two years. The score ranges from 1 to 100 (1 being the worst, and 100 being the best) and is commonly used by creditors to assess creditworthiness.

PAYDEX® score model.

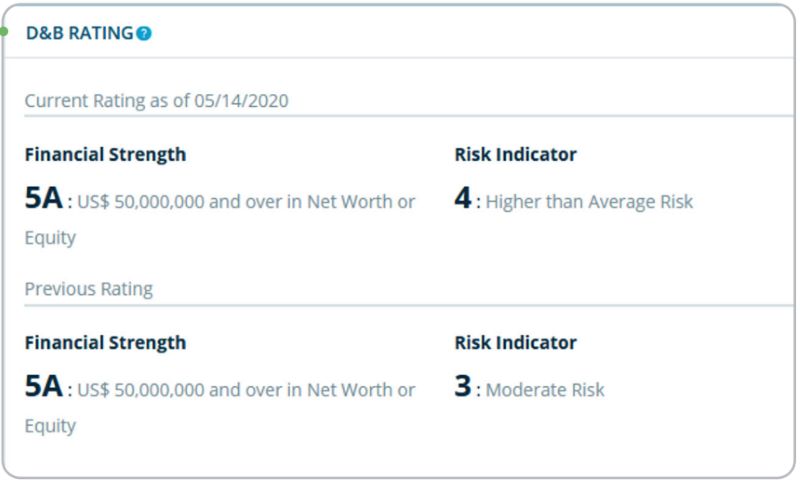

5. D&B RatingA D&B rating is an average of a company’s historical financial performance inclusive of payment history, business age and size, and other financial information. The rating is shown as an alphanumeric figure, representative of financial strength and risk indicators.

D&B rating model.

The trade payments section summarizes payment history to other partners. It indicates evidence of payment behavior, such as past-due amounts and total days of past-due payments. Also noted are the types of trade accounts and the total value of each tradeline.

Trade Payments section of a D&B profile.

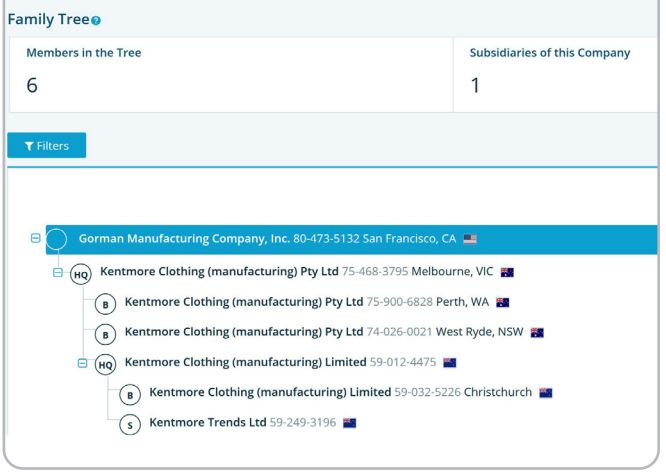

This section provides an overview of the ownership chart, which displays relationships between different companies in the D&B database.

This can be utilized to assess potential risk across a family tree alongside providing a global overview of the majority-owned subsidiaries and their relationships.

Ownership section of a D&B profile.

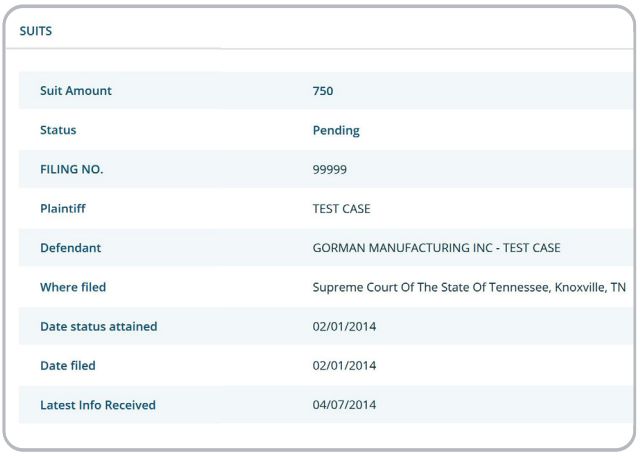

The legal events section reports any legal activity that could impact the financial stability of your business, such as bankruptcy filings, judgments, liens, lawsuits, and UCC filings.

Legal Events section of a D&B profile.

Details regarding any legal events are summarized as demonstrated in the example below:

Example of legal events summary.

The Special Events section presents the latest developments of a business, such as changes in ownership, operations, and earnings announcements, if applicable.

Special Events section of a D&B profile.

Depending on the company, documentation, such as balance sheets, cash flow records, and profit and loss (P&L) statements among other financial reports, can be accessed via a D&B credit report.

Financials section of a D&B profile.

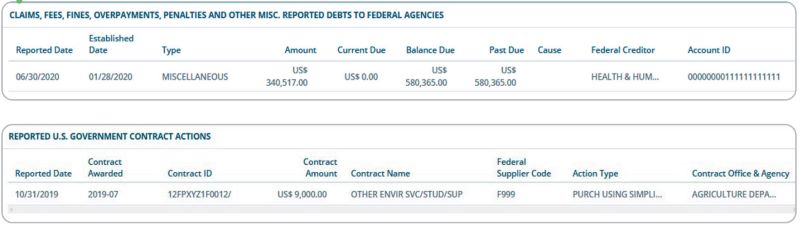

This section supplies information regarding dealings with the US government (including exclusions) and highlights any activity, such as contracts, debts, or assistance.

Federal Information section of a D&B profile.

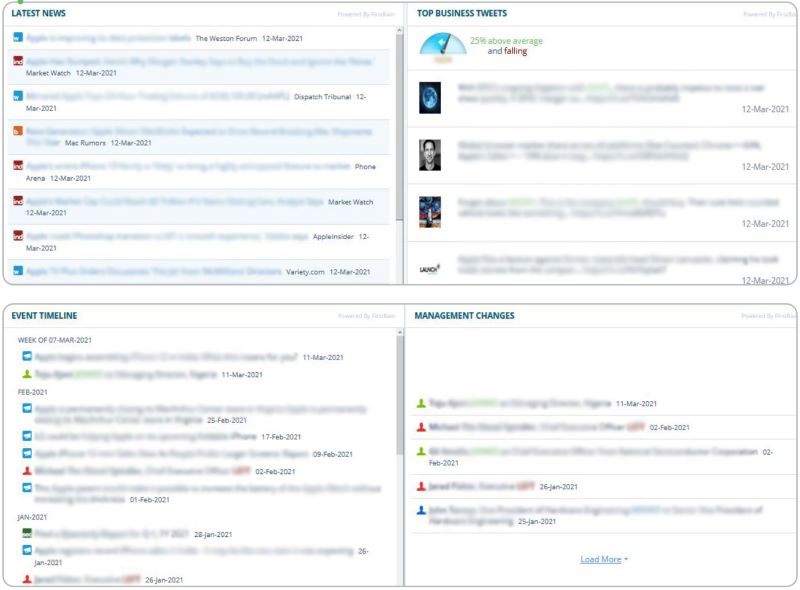

The Web & Social section generally reports on the latest news and any publications that may reference your business. This is useful in painting a picture to anyone researching your company, or assisting in the explanation of potential risks.

Web & Social section of a D&B profile.

News reporting rumored events have no impact on a D&B credit score.| PROS | CONS |

|---|---|

| Is a popular and trusted source | Can be costly, especially for small businesses |

| Is required from lenders and for government contracts | Requires you to get a DUNS number, which can take up to 30 days |

| Helps you monitor and build credit for your business | Requires you to maintain your business profile, which can be costly |

D&B collects data and compiles it into a variety of scores and ratings on a credit report to demonstrate the financial wellbeing of your business. These include factors, such as company structure, payment history, and legal events. Your business profile is publicly available, and your creditworthiness can be evaluated by creditors, partners, or vendors who may be interested in working with you. Numerous report types are available and the information included will differ depending on your choice of report.

D&B credit reports are accessible to all businesses and can be obtained from the D&B website:

While the Dun & Bradstreet credit report is one of the most trusted financial resources, there are other options available that can provide you with similar metrics and insights.

The D&B report includes a score of 0 to 100, and the higher the score, the better. A score of 80 or above indicates a business is low risk, is reliable, and makes payments on time.

Can I get a D&B credit report for free?Yes. D&B Credit Insights provides a free credit report that you can utilize to check your scores and monitor any changes.

How can I correct or modify a D&B report?If you believe there may be an error on your report, use the D-U-N-S Manager form or contact Dun & Bradstreet directly.

A Dun & Bradstreet Credit Report uses data collected from your business history to provide scores that determine your business’s creditworthiness. The report is utilized by creditors and partners to determine the history and reliability of your business. It is a useful tool for applying for a small business loan, monitoring your credit, or leveraging your credibility for better terms.

Lauren McKinley is a Staff Writer at Fit Small Business, specializing in Finance. She’s a financial professional with over 4 years of diverse experience in the banking industry, primarily in the Northeast. Her expertise spans roles as a Credit Analyst, Loan Administrator, and Bank Teller, obtaining skills in commercial real estate, financial analysis, and banking operations. With a particular focus in small business financing, she has navigated financial solutions for a variety of lending institutions.